The Harder Trail: Why FINE is the Adventure Worth Taking

The Harder Trail

I was at a conference recently, and one afternoon we had an unexpected long break. Most people used it to network, catch up with colleagues, or head to the golf course. Nothing wrong with golf — but I wasn’t craving manicured lawns or polite conversation. I wanted the wilds. I wanted space to think. I wanted to get my heart pumping.

So I drove to a nearby trailhead and planned a simple one‑hour loop. Just enough to clear my head.

About twenty minutes in, I saw a trail shooting straight up the ridge. A steep incline. Sharp switchbacks. Towering desert plants silhouetted against a sky so blue it looked infinite.

It looked harder — and more interesting.

I paused, took a breath, and decided to go for it.

What was supposed to be a one‑hour loop turned into a 2.5‑hour adventure. And as I climbed, I felt something I hadn’t felt in a long time: that youthful spark of spontaneity. It reminded me of being in my early twenties, hiking up into the Blue Ridge Mountains in the snow with a group of buddies — pitching a tent in freezing weather, drinking a couple beers, staring at the stars, doing the kind of frivolous, beautiful, slightly stupid things you only do when you’re young.

And somewhere on that ridge, a thought hit me:

Some paths are harder now but lead to a more meaningful second half of life.

That’s what FINE is.

If you want the backstory behind what pushed me toward this path, I wrote about the moment everything shifted.

The Easy Loop vs. The Harder Trail

Most of us are offered two paths.

The Easy Loop

The easy loop is traditional retirement — work until 65, then pickleball, golf, and beach. Comfortable, predictable, familiar. Nothing wrong with it.

The Harder Trail

The harder trail is something different. It means pursuing a Next Endeavor — staying mentally sharp, using gifts you've spent decades developing, and contributing in ways that actually matter. It's not retirement from life. It's retirement from the wrong work.

The tension is simple: comfort versus calling. Ease versus meaning. Escape versus contribution.

FINE lives on the harder trail — the one that requires more effort but leads somewhere better. I wrote about how I discovered FINE and what it means in practice in How FI Led Me to FINE.

The Problem: Most Americans Are Behind

A few quick stats from Vanguard, Fidelity, and the Federal Reserve:

The median 401(k) balance for Americans in their 50s ranges from $68K to $96K — far short of what most people need.

The average personal savings rate in the U.S. is 7.7%.

36% of non-retired Americans have $0 saved for retirement.

Only 14% of workers max out their 401(k).

Most people can’t save 40–50% of their income to FIRE.

And many don’t want to retire at 40 and never work again.

They want meaning.

They want flexibility.

They want adventure.

They want to use their gifts.

They want FINE.

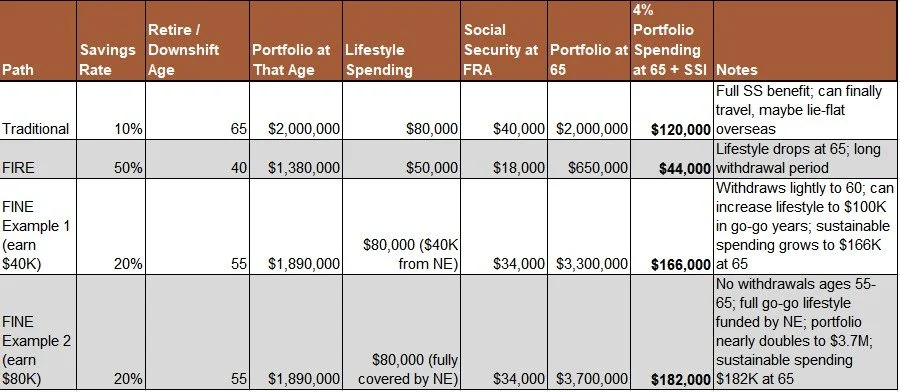

The Three Paths: Traditional vs. FIRE vs. FINE

To keep the comparison simple and focused on the differences between the three paths, I’m using a flat $100K income. In real life, incomes rise over time — but the relationships between these paths stay the same.

Here’s what happens when three people earning the same income choose different paths.

Traditional vs FIRE vs FINE:

Assumptions: $100K income, 7% real returns. FINE Examples assume a next endeavor beginning at 55. Portfolio projections use Monte Carlo simulation medians at 7% nominal returns. Sustainable spending at 65 = 4% of portfolio + Social Security at Full Retirement Age (FRA). Actual results will vary based on sequence of returns and market conditions.

A note on income: These examples use $100K to keep the math clean and the relationships visible. But the FINE concept scales powerfully at higher incomes. For example, a Next Endeavor generating $80K doesn’t just hedge sequence of returns risk — it funds a dramatically different lifestyle in the early retirement years while the portfolio compounds untouched. The gap between $170K from portfolio withdrawals and $250K supported partly by meaningful work isn’t just financial. It’s the difference between a good retirement and a great one. The math scales. So does the life.

What the Table Really Means

Traditional

The traditional saver works until 65, lives a normal life, and ends up with $2M— proportionally more at higher incomes.

Because Social Security covers roughly half their spending, they actually get a raise in retirement. They can finally travel, maybe even splurge on lie‑flat business class once or twice.

But they’re in the 9th inning of life.

They missed out on 10 years of energy, travel, and freedom.

FIRE

The FIRE saver hits their number at 40 — but only by living on $50K forever.

They also get a much smaller Social Security benefit because they only worked about 18 years.

From 40 to 65, they withdraw the $50K they’re used to.

By age 65, their nest egg has shrunk to roughly $650K.

At 67, Social Security kicks in (~$18K).

But even with that, their sustainable spending is:

$26K (4% of $650K)

$18K Social Security

= $44K total

That’s below the $50K lifestyle they’ve maintained for 27 years.

Mathematically possible.

Emotionally and financially fragile.

FINE Example 1: Earn $40K in a Next Endeavor

The FINE saver downshifts at 55, earns $40K doing something meaningful, and only needs to withdraw $40K from their portfolio for five years.

Their portfolio still grows — ending at $3.3M by age 65.

At 60, they can actually increase their lifestyle from $80K to $100K because the portfolio is compounding faster than they’re withdrawing.

This is the power of avoiding early withdrawals and giving your money 10 extra years to grow.

FINE Example 2: Earn $80K in a Next Endeavor

If their next endeavor earns closer to $80K, they don’t need to withdraw anything.

Their portfolio compounds untouched and nearly doubles to $3.7M.

The punchline:

FINE gives you back 10 years of compounding — the decade where money doubles — while letting you live on 3–4× the FIRE lifestyle.

Real Stories From the FINE Trail

My Dad

My dad was a writer and eventually editor‑in‑chief of a defense periodical.

He loved writing — but not office politics, deadlines, or someone else’s priorities.

When he stepped away from full‑time work, he took only the projects he wanted.

He took months off at a time.

Summers in DC were too hot, so he wrote more.

Spring and fall he worked less.

He built a life around seasons, not schedules.

He wasn’t wealthy — he just had time, flexibility, and a knack for making the most of opportunities.

He wrote a book, did consulting, appeared on TV programs, and took my mom to Ireland for several weeks. He went to the Paris Air Show and wrote it off as a business expense — something he would’ve loved to do anyway.

That’s FINE.

Jenny

A friend from a city we used to live in.

Her husband retired from banking.

She always loved travel.

So she became a travel planner.

Now she helps friends plan trips to Europe, the Caribbean, and beyond. She gets discounts and upgrades on her own adventures. And she lights up when she talks about helping people create memories.

That’s FINE.

Betty

Betty goes to my church.

Her savings were modest and slowly running out.

She loved sewing — used to make custom curtains and even wedding dresses.

Now she sells beautiful handmade pieces at craft shows a few times a year.

It brings her joy and gives her dignity.

And a few thousand dollars a year changed everything.

That’s FINE.

Why the Harder Trail Is Worth It

FINE gives you meaning and margin — the breathing room to make decisions from clarity instead of fear. It gives you flexibility and freedom, the ability to travel, rest, and explore on your own schedule. It gives you a chance to contribute — to use gifts you've spent decades developing in ways that actually matter. And it keeps you sharp, engaged, and building wealth, often more than either Traditional or FIRE.

You don't have to retire from life to retire from your job.

You can travel.

You can rest.

You can explore.

You can use your gifts.

You can stay sharp and engaged.

The Invitation

If you’re in that in‑between space — not done, not finished, but ready for something more meaningful — FINE is for you.

You don’t need to overhaul your life.

You just need to take the next step.

Explore your next endeavor.

Choose the trail that leads somewhere meaningful.

If you're just finding Desert FI, Fresh Tracks picks up where this post leaves off — a glacier, an avalanche blast at dawn, and the question of whose tracks you've been following.

If this resonated, please share it with someone who’s wrestling with their next chapter.

And if you want more stories, math, and meaning each week — subscribe to Desert FI Weekend Reflections below.

Let’s take the harder trail together.

🌵Desert FI

Geek Out Corner:

For readers who like to see the numbers, below are the Monte Carlo outcomes using randomized, historic market returns.

Traditional: ~95% success rate

FIRE: ~70% (long withdrawal period + small SS benefit)

FINE Example 1: ~98%

FINE Example 2: ~99%+

Was this just because the savings rate doubled?

No.

If someone saved 20% but fully retired at 55 (no next endeavor), their success rate would be around 75–80%.

With a next endeavor (FINE Example 1), success jumps to 98%.

With no withdrawals at all (FINE Example 2), success jumps to 99%+.

Conclusion:

The next endeavor — not the savings rate — is what drives the massive increase in success.

Avoiding early withdrawals is the real engine of FINE.